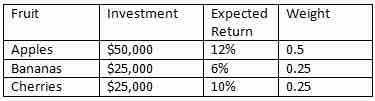

Let's say that we have a portfolio that consists of three assets, and we'll call them Apples, Bananas, and Cherries. We decided to invest in all three, because the previous chapters on diversification had a profound impact on our investment strategy, and we now understand that diversifiable risk doesn't pay a risk premium, so we try to eliminate it.

A Fruitful Portfolio

How would you calculate the expected return on this portfolio?

The return of our fruit portfolio could be modeled as a sum of the weighted average of each fruit's expected return. In math, that means:

Where A stands for apple, B is banana, C is cherry and FMP is farmer's market portfolio. W is weight and E(RX) is the expected return of X. A good exercise would be to calculate this figure on your own, then look below to see if you completed it accurately.

Here's what you should get:

In reality, a portfolio is not a fruit basket, and neither is the formula. A math-heavy formula for calculating the expected return on a portfolio, Q, of n assets would be:

What does this equal?

Remember that we are making the assumption that we can accurately measure these outcomes based on what we have seen in the past. If you were playing roulette at a casino, you may not know if red or black (or green) is coming on the next spin, but you could reasonably expect that if you bet on black 4000 times in a row, you're likely to get paid on about 1900 of those spins. If you go to Wikipedia, you can review a wide variety of challenges to this model that have very valid points. Remember, the market is random: it is not a roulette wheel, but that might be the best thing we have to compare it to.