Theory of Constraints

All processes are susceptible to constraints; the theory of constraints (TOC) postulates that "the chain is only as strong as its weakest link." Because systems are interdependent, it makes sense that an entire set of processes within an operational paradigm can be made vulnerable to failure by a single process that is struggling.

TOC assumes that throughput, operational expense, and inventory are the three central inputs in a given system. TOC relies on the assumption that there is always room for improvement in these inputs–after all, if there was nothing preventing the system from achieving higher throughput, throughput would be infinite.

This means that any time organizations encounter substantial internal or external constraints, it is the role of management to create a strategy to circumvent them. Since throughput is never infinite, this is an ongoing process.

Internal Constraints

At the organizational level, internal control objectives concern the reliability of financial reporting, timely feedback on the achievement of operational or strategic goals, and compliance with laws and regulations. With this in mind, we can summarize internal constraints as any one or any combination of the following:

- Equipment: The way equipment is used limits the ability of the system to produce more salable goods/services.

- People: Lack of skilled people limits the system; mental models also cause negative behaviors that become constraints.

- Policy: A written or unwritten policy prevents the system from making more goods/services.

The list of potential internal constraints is long: employees may not have the proper skills to use specific types of equipment, policy may organize the processes in an imperfect manner, equipment may depreciate faster than expected, employees may be absent or inefficient, policy may limit resource allocation to inventory and warehousing, etc. Internal constraints are a constant concern for the managers who must try to minimize them by continually optimizing the system. For example, if employees lack specific skills, management may want to refine its hiring policies.

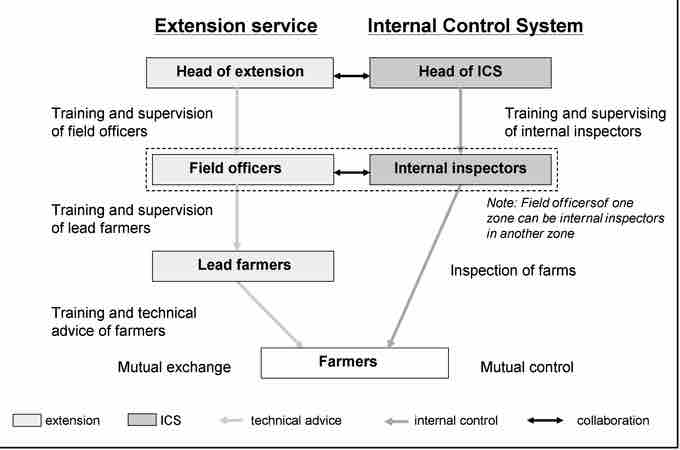

Internal control system

This flowchart illustrates how an internal control system can be integrated into the production process: mid-level managers of one department can monitor and QA other departments' output.

External Constraints

In their attempts to maximize existing profits, business managers must consider both the short- and long-term implications of decisions made within the firm and the various external constraints that could limit the firm's ability to achieve its organizational goals. These constraints can be organized into three categories:

- Scarcity

- Contracts

- Legalities

The first external constraint, resource scarcity, refers to the limited availability of essential inputs (including skilled labor), key raw materials, energy, specialized machinery and equipment, warehouse space, and other resources. Moreover, managers often face constraints on plant capacity that are exacerbated by limited investment funds available for expansion or modernization.

Contractual obligations also constrain managerial decisions. Labor contracts, for example, may constrain managers' flexibility in worker scheduling and work assignments. Labor contracts may also restrict the number of workers employed at any time, thereby establishing a floor for minimum labor costs.

Finally, laws and regulations have to be observed. Legal restrictions can constrain production and marketing decisions. Examples of laws and regulations that limit managerial flexibility include: minimum wage, health and safety standards, fuel efficiency requirements, anti-pollution regulations, and fair pricing and marketing practices.